5 June 2026

by Beutel Goodman Fixed Income Team

The Canadian economy has slipped into what is known as a technical recession. Two consecutive quarters of negative annualized growth (down -1.0% in Q4 2025 and -0.1% in Q1 2026) fits the familiar rule-of-thumb definition and is certainly enough to attract attention.

But this current episode feels different. The key question is not whether Canada meets a technical definition; it is whether the underlying data signals point to an economy that is breaking down or simply slowing in a more uneven way. Beneath the surface, the data points to something more nuanced than a broad-based downturn.

Trade, Inventories and a Noisy GDP Signal

The recent weakness in GDP is best understood as a function of inventory and trade dynamics rather than a domestic recession. The distortions have changed from quarter to quarter, but the broader point is the same: headline GDP has been noisier than usual.

In Q4 2025, the main drag came from a decrease in inventories, particularly in manufacturing. On the surface, that looked negative for growth. But an inventory drawdown is not always a bad signal. If it reflects stronger sales rather than weaker production, it can point to firmer demand. Seen in that light, the negative GDP print in Q4 looked less worrisome than the headline implied.

In Q1 2026, the pattern reversed. Inventories rebuilt and added meaningfully to GDP. At the same time, imports surged and exports softened. Because GDP measures domestic production, strong imports subtract from growth mechanically even when they reflect underlying demand, and that was enough to tip headline GDP into negative territory.

Even the inventory rebuild and the spike in imports in Q1 need to be interpreted with care. Under normal circumstances, an inventory build can suggest softer end demand. But this episode was different. Nearly half of the first-quarter increase came from gold inventories following a surge in gold imports, which makes this look more like a trade-related distortion than a sign of domestic weakness. By contrast, retail and wholesale inventories declined in the quarter, suggesting demand in those sectors may have held up better than headline GDP implied.

What links the two quarters is that both were shaped by unusually volatile trade and inventory dynamics. Since Liberation Day, geopolitical tensions, tariff uncertainty and the run-up in gold prices have made headline GDP a less reliable guide to underlying domestic demand.

Finding a Truer Growth Signal

Can we infer nothing from the GDP data simply because the headline is distorted by swings in exports, imports and inventories? Not quite. Final domestic demand offers a cleaner read on underlying momentum because it excludes both net trade and inventory effects.

By that measure, the economy looked considerably less weak. Final domestic demand rose at a 2.7% annualized pace in Q4 2025 and then slipped to -0.4% annualized in Q1 2026. That points more to stagnation than to a broad-based recession. Even within that softer Q1 reading, much of the weakness came from a temporary decline in government spending rather than a generalized deterioration in private-sector demand.

Another useful question is: what did not weaken? What stands out is household Final Consumption Expenditure. The measure of household spending continued to edge higher in Q4 2025 by a robust 2.9% quarterly annualized and also up in Q1 2026 at 1.5% quarterly annualized.

If this were a classic recession, consumption would be leading the decline. Instead, it continues to act as a stabilizing force. Household spending remains the largest anchor of economic activity, particularly on the services side, where labour income makes up the largest share. Across economist forecasts, consumer demand is still expected to remain strong through 2026. Another positive signal is Statistics Canada’s advance estimate that real GDP rose 0.4% in April, pointing to a firmer start to Q2 2026.

At the same time, population dynamics are becoming more important in interpreting the data. With population growth slowing and even turning negative in recent quarters, aggregate GDP becomes a less reliable gauge of underlying momentum. In fact, GDP per capita rose at a quarterly annualized pace of 0.9% during Q1 2026.

That distinction matters. A decline in aggregate GDP driven by population effects and external trade does not carry the same implications on an individual level as a broad pullback in per-capita demand. In that sense, the current episode is the mirror image of 2023 and 2024, when strong population growth helped keep headline GDP positive even as per-capita GDP was weakening. Today, the economy may be underperforming, but it is not experiencing the kind of widespread contraction typically associated with recession.

Monetary Policy and the Reaction Function

For markets, an important question is how policymakers interpret the data. On this front, the Bank of Canada has been clear. As Senior Deputy Governor Carolyn Rogers said on June 1, “we need to be careful not to put too much weight on any one indicator.” GDP matters, but it is not the main driver of decisions. The Bank’s framework is anchored by a 2% inflation target, with inflation and labour market conditions at the centre of the reaction function.

Those signals point to an economy that is cooling but not collapsing. CPI inflation rose to 2.8% in April 2026 from 2.4% in March, but most of that increase came from energy-related components. Core inflation remains much closer to target.

The labour market also argues for caution, not panic. The unemployment rate was 6.9% in April 2026, and Bank of Canada officials have described conditions as soft rather than in crisis. Job growth has stagnated year to date, but part of that reflects weather-related disruptions in sectors such as construction as well as weaker labour supply after population growth turned negative. That reinforces the idea that the recent softness is not purely a demand-side slowdown.

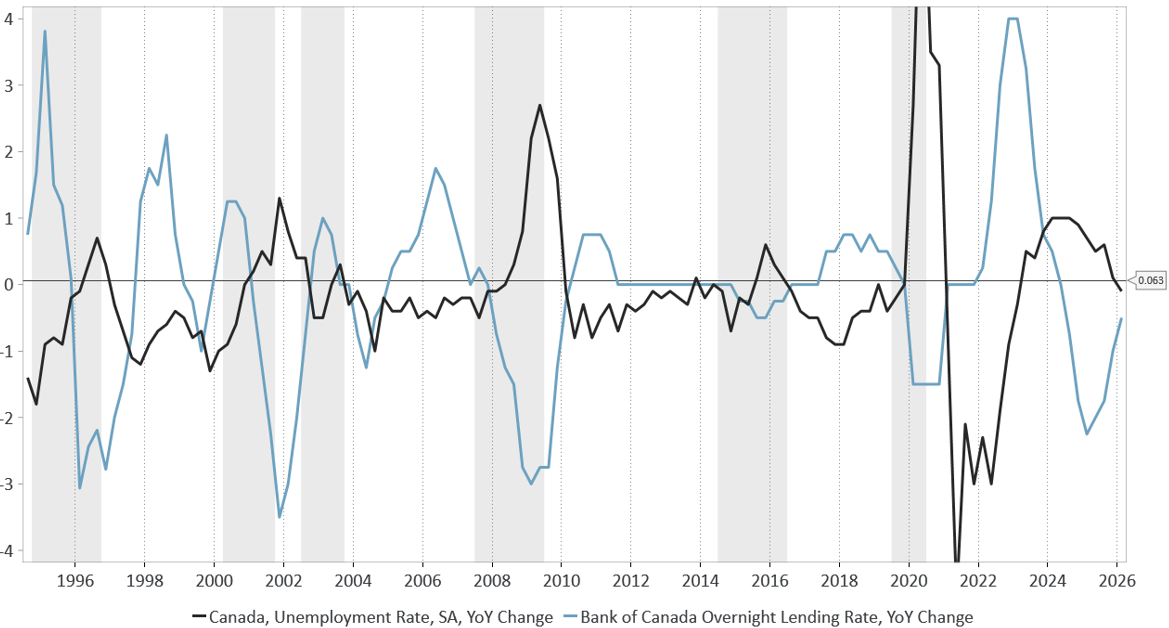

Chart 1 reinforces why labour matters so much for policy. Historically, the Bank of Canada has responded far more directly to labour market deterioration than to GDP headlines alone. Periods of rising unemployment have generally coincided with falling policy rates. More recently, however, the year-over-year change in unemployment has been relatively stable and has even edged slightly lower over the past 12 months.

Chart 1. The Bank of Canada Reacts to Labour Market Weakness: The line chart compares the year-over-year change in Canada’s unemployment rate and the Bank of Canada overnight lending rate from the mid-1990s to 2026, showing that periods of rising unemployment generally coincide with falling policy rates.

As of 2026-06-03

Sources: Beutel, Goodman & Company Ltd., Statistics Canada

Canada’s trade weakness is also concentrated rather than broad-based. Resource exports have held up, while non-resource exports remain sluggish. That helps explain why headline growth looks soft even as parts of the external sector continue to perform reasonably well.

As we argued in last month’s Central Bank Conundrum, this mix should keep the Bank of Canada on hold for now. With inflation near target, and labour markets soft but not breaking, the case for a near-term policy change remains limited.

The Outlook: Bending, Not Breaking

Looking ahead, most forecasts still point to modest growth for 2026, with several supports beginning to emerge.

First, trade uncertainty may begin to ease at the margin. Even a partial or temporary resolution around the United States-Mexico-Canada Agreement (USMCA) would remove a key drag on business confidence and investment. The current environment has been defined as much by uncertainty as by tariffs; the removal of that uncertainty would be additive to growth even if trade barriers remain in place.

Second, fiscal policy is starting to turn more supportive. Recent budget measures and increased public spending are expected to feed through gradually, particularly in infrastructure and strategic sectors. In a slow-growth environment, this type of spending can help offset private sector caution.

Third, spillovers from U.S. fiscal policy remain an underappreciated tailwind. Continued strength in the U.S. economy, supported in part by fiscal expansion, should support external demand for Canadian exports, particularly as trade relationships stabilize.

Finally, commodity dynamics continue to work in Canada’s favour. Higher energy prices are lifting national income and supporting government revenues, even if the benefit is uneven across households and regions. Higher energy prices are a mixed blessing. They squeeze consumers, but they also improve Canada’s terms of trade, and support national income.

Housing, in particular, illustrates the balance in the outlook. Conditions appear to have stabilized rather than continuing to deteriorate. Activity remains subdued and affordability constraints persist, but the weakness is not evenly distributed across the country. Much of the drag is concentrated in Ontario and British Columbia, especially in Toronto and Vancouver, where elevated inventories, particularly in the condo market, continue to weigh on prices and turnover. By contrast, markets such as Montreal and Calgary have been more resilient. Overall, that is more consistent with housing acting as a drag in specific pockets than with a broad national recession signal.

Weak GDP has not yet translated into broad financial stress. That matters because recessions become more damaging when weak growth turns into tighter financial conditions and meets a fragile private-sector balance sheet.

Taken together, the forward-looking picture is one of stabilization as the year progresses.

The Path Ahead

Canada may be in a technical recession, but the label tells only part of the story. Trade and inventory distortions, along with weaker population growth, have weighed on headline GDP without producing the kind of domestic contraction usually associated with recession.

Household consumption has held up, and per capita GDP has been firmer than the headline suggests. That said, stabilization does not mean immunity. Once an economy loses positive momentum, the margin for error becomes thinner and vulnerability to new shocks rises.

The labour market is especially important here because of its reflexive nature. If job losses begin to mount, then households cut spending, weaker spending feeds back into growth, and the risk of a more self-reinforcing downturn rises. For fixed income investors, a relevant question is whether the underlying drivers of growth, especially labour, are beginning to deteriorate in a meaningful way. So far, the evidence still points to an economy that is slowing, but functioning, with scope for a more stable second half of the year. That is why labour remains the most important signal to watch in the months ahead.

Download PDF

Related Topics and Links of Interest:

©2026 Beutel, Goodman & Company Ltd. Do not sell or modify this document without the prior written consent of Beutel, Goodman & Company Ltd. This commentary represents the views of Beutel, Goodman & Company Ltd. as at the date indicated. This document is not intended, and should not be relied upon, to provide legal, financial, accounting, tax, investment or other advice.

Certain portions of this report may contain forward-looking statements. Forward-looking statements include statements that are predictive in nature, that depend upon or refer to future events or conditions, or that include words such as “expects”, “anticipates”, “intends”, “plans”, “believes”, “estimates” and other similar forward-looking expressions. In addition, any statement that may be made concerning future performance, strategies or prospects, and possible future action, is also forward-looking statement. Forward-looking statements are based on current expectations and forecasts about future events and are inherently subject to, among other things, risks, uncertainties and assumptions which could cause actual events, results, performance or prospects to be incorrect or to differ materially from those expressed in, or implied by, these forward-looking statements.

These risks, uncertainties and assumptions include, but are not limited to, general economic, political and market factors, domestic and international, interest and foreign exchange rates, equity and capital markets, business competition, technological change, changes in government regulations, unexpected judicial or regulatory proceedings, and catastrophic events. This list of important factors is not exhaustive. Please consider these and other factors carefully before making any investment decisions and avoid placing undue reliance on forward-looking statements Beutel Goodman has no specific intention of updating any forward-looking statements whether as a result of new information, future events or otherwise.