21 February 2025

Summary

Trade tensions between the U.S. and Canada have dominated the news cycle in the early stages of 2025. In this piece, the Beutel Goodman Fixed Income team looks at the changing relationship between the two countries and how economic and political forces are contributing to divergence on interest rates and currency valuations between these North American neighbours.

By Beutel Goodman Fixed Income team

“…it was the season of Light, it was the season of Darkness, it was the spring of hope, it was the winter of despair, we had everything before us, we had nothing before us…” Charles Dickens, A Tale of Two Cities

In June 2024, we explored aspects of Canada’s economic relationship with the United States in our Insight piece: A Tale of Two Countries: Economic Divergence in North America. Since then, this topic has become increasingly relevant, as economic conditions continue to diverge and interest rate and currency differences between the two neighbours are elevated. Donald Trump has returned to the Oval Office, casting a looming threat of tariffs and a trade war over Canada’s economic prospects. Canada, meanwhile, will soon elect a new prime minister following the resignation announcement of Justin Trudeau in January.

We therefore present: A Tale of Two Countries Part 2, with more insights on this topic and an analysis of what may be in store for the rest of 2025.

Two Neighbours on a Different Path

Looking back to June 2024, the month stands out as the Bank of Canada (BoC) became the first central bank in the G7 to reduce its policy rate since the tightening cycle began in 2022. The BoC’s dovish pivot was aimed at supporting a weakening Canadian economy, which had been heavily impacted by the interest rate hikes of 2022 and 2023. Canada has a heightened degree of interest rate sensitivity due to higher household debt levels and differences in its mortgage market.

The Canadian housing market is dominated by variable-rate mortgages and five-year fixed-rate mortgages that often have stiff prepayment penalties. As mortgage rates increased materially since 2022, the new higher rates meant that homeowners have had less disposable income to spend on other goods and services.

In the U.S., mortgages are skewed to 30-year fixed rates, which allows U.S. mortgage holders the option to keep their existing contracted rate for a 30-year period. This made U.S. homeowners much less sensitive to U.S. Federal Reserve (Fed) rate hikes in 2022/2023 and the impact on household spending was less pronounced.

Since June 2024, the BoC has reduced its policy rate at each of its meetings to the current level of 3.00%, set in January 2025. In the U.S., the Fed has been less aggressive in reducing the Federal Funds Rate, making its first cut (of 50 bps) in September 2024, with cuts of 25 bps at each of its November and December meetings, before pausing at its January meeting with the target range at 4.25-4.50%. This means that the difference between the key lending rates for the BoC and the Fed (using its upper bound) has grown to 150 bps.

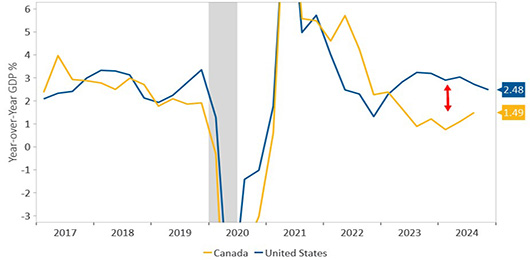

Historically, Canada’s central bank has been reluctant to diverge too far from Fed policy, but the difference in rates today reflects the contrasting economic conditions in the two countries. Real GDP (gross domestic product) has been higher in the post-COVID period in the U.S. versus Canada (see Exhibit 1), led in large part by a high degree of consumer confidence and robust spending in the U.S. High immigration levels and the associated boost in consumption played a large part in Canada avoiding a recession in 2024; however, there have been some meaningful second-order impacts from these factors. For example, on a per-capita basis in Canada, real GDP has been negative for the last seven quarters, meaning that the average person’s experience has been recession-like, with unemployment climbing and a decline in consumer confidence.

Exhibit 1: U.S. & Canada GDP. The chart below shows how the economic performance between the U.S. and Canada has diverged since the end of the pandemic.

Chart represents period from January 31, 2017 until January 31, 2025.

Source: Beutel, Goodman & Company Ltd. U.S. Bureau of Economic Analysis (BEA), Statistics Canada.

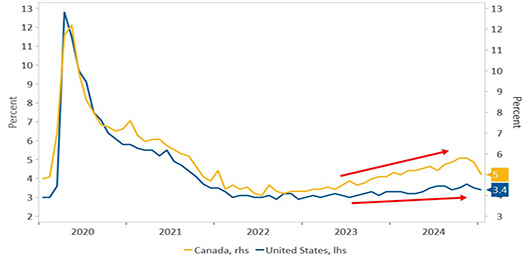

The increased pool of workers has also not been fully absorbed into the jobs market and the unemployment rate in Canada ended 2024 at 6.7%, compared to 4.1.% in the U.S. (see Exhibit 2). Private sector employment growth has been especially weak in Canada, with employment in the public sector making outsized contributions to job gains.

Exhibit 2: U.S. & Canada Job Market. This chart shows the divergence in unemployment rates (for the prime age 25 to 54 years).

Chart represents period from January 31, 2020 until January 31, 2025.

Source: Beutel, Goodman & Company Ltd. U.S. Bureau of Economic Analysis (BEA), Statistics Canada.

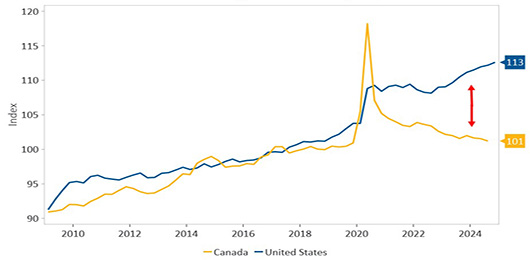

With the pool of available workers rising, the average output per worker, a measure of labour productivity, has fallen in recent years. The diverging productivity rates show that Canada’s business sector is operating less efficiently than in the U.S. (see Exhibit 3).

Exhibit 3: U.S. & Canada Productivity. This chart shows the Labour Productivity of the U.S. relative to Canada trending lower and the U.S. trending higher.

Chart represents period from March 31, 2009 until January 31, 2025.

Source: Beutel, Goodman & Company Ltd. U.S. Bureau of Economic Analysis (BEA), Statistics Canada.

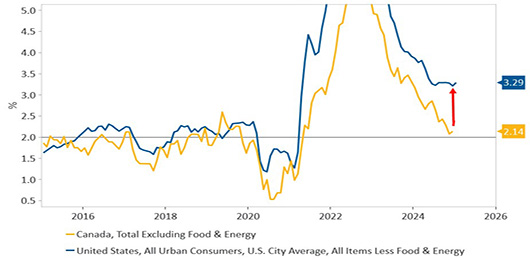

The recent trajectory of consumer price inflation is also diverging between the U.S. and Canada. Inflation in Canada is close to the Bank of Canada’s 2% target, reflecting an economy that is running at a slower pace (see Exhibit 4). U.S. inflation has been considerably stickier, as the robust consumer backdrop means that firms still have the ability to pass on price increases.

Exhibit 4: U.S. & Canada Inflation. This chart shows the divergence between the seasonally adjusted (SA) Consumer Price Index, excluding food and energy, which is the most common reading for core inflation. Canada is close to the Bank of Canada’s 2% for inflation.

Chart represents period from January 31, 2015 until January 31, 2025.

Source: Beutel, Goodman & Company Ltd. U.S. Bureau of Economic Analysis (BEA), Statistics Canada.

Economic divergence has further intensified in recent months amid strong pro-growth sentiment in the U.S., in addition to the effect of the Trump administration’s policies on deregulation, sustained tax cuts and trade protectionism.

On February 1, 2025, President Trump announced through the International Emergency Economic Powers Act an executive order to impose 25% tariffs on all imports from Canada (and other countries), with the exception of energy, which would have a 10% tariff. Subsequently, Canada announced retaliatory counter-tariffs on targeted U.S. goods, all of which would go into effect on February 4. However, both sides agreed to delay the onset of tariffs by 30 days, pending a commitment by Canada to bolster border security against the flow of illegal drugs and migrants to the U.S.

On February 11, the Trump administration revived a contentious trade policy from its previous term in office, announcing 25% tariffs on all U.S. imports of steel and aluminum products, scheduled to come into effect on March 12.

It is difficult to know if further tariffs will ultimately come to pass, or if the threats are a negotiating tactic designed to produce more concessions from trading partners. We also cannot fully anticipate the extent and impact of retaliatory measures or the fiscal response to an escalation in trade tensions.

The U.S. is Canada’s largest trading partner by far, so tariffs, in addition to retaliatory counter-tariffs, have the potential to be immensely damaging to Canada, and put upward pressure on inflation and downward pressure on growth. The uncertainty surrounding the tariff situation in itself is enough to weigh on an already weakening business and economic environment, which could further the economic divergence with the U.S.

Impact of Divergence

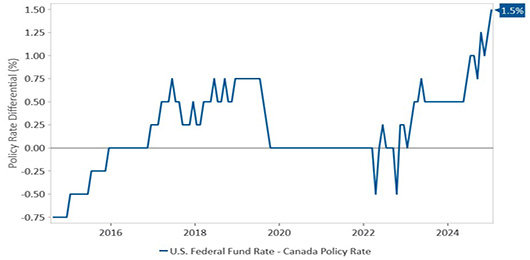

The gap between the BoC and Fed policy rates (see Exhibit 5), in conjunction with the diverging economies, have elevated the differential between 10-year government bond yields between the two countries (see Exhibit 6). This disparity has meant the value of Canada’s loonie has sunk in recent months, hovering around US$0.69 at the end of January. A weak Canadian dollar could benefit exporters in need of a boost should stiff tariffs be enacted, but is costly for businesses or consumers importing goods from the U.S.

Exhibit 5: U.S.-Canada Interest Rate Divergence. The chart below shows the difference between the policy rates of the Fed and the BoC.

Chart represents period from August 31, 2014 until January 31, 2025.

Source: Beutel, Goodman & Company Ltd. U.S. Department of Treasury, Macrobond Financial AB, Federal Reserve, Bank of Canada.

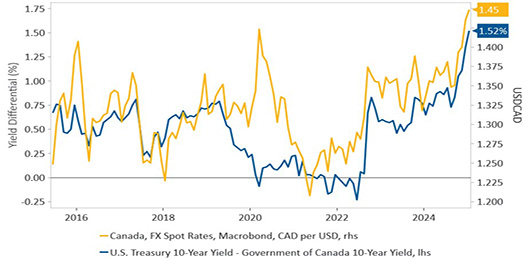

Exhibit 6: U.S.-Canada Yields. U.S.-Canada Yields. This chart shows how the yields of the 10-Year U.S. Treasury and the 10-Year Government of Canada Bond have diverged. The chart also shows the correlation between the interest rate divergence and the weakness in the Canadian dollar (how the yellow line and the blue line largely move together).

Chart represents period from June 30, 2015 until January 31, 2025.

Source: Beutel, Goodman & Company Ltd. U.S. Department of Treasury, Macrobond Financial AB, Federal Reserve, Bank of Canada.

The differential in bond yields between Canada and the U.S., and the weakening effect this is having on the value of Canadian currency, places the Bank of Canada in a difficult position. A weaker currency is inflationary due to the impact of higher import costs; therefore, should the Canadian economy need monetary stimulus in 2025, the impact of lower policy rates may be counterproductive.

Currently, the policy rate in Canada sits close to the BoC’s estimate of the neutral rate for the economy (i.e., neither stimulative nor restrictive, see also Exhibit 4), while the Fed rate remains well above its neutral rate estimate. It is likely that the BoC will move more into stimulative territory in 2025, but not significantly given the currency implications for continuing its aggressive rate-cutting cycle.

Fiscal support from federal and provincial governments may be needed to pick up the economic slack. This warrants caution, however. Canada is held to much stricter standards in terms of acceptable fiscal deficits than the U.S., which benefits from its position as the world’s reserve currency. We have already seen bond markets push back against fiscal largesse in countries such as the U.K., where a proposal in 2023 to lower taxes funded by borrowing resulted in a sharp increase in rates and an aggressive currency devaluation.

The Case for Continued Divergence

The current divergence of policy rates between the U.S. and Canada is not typical for the two countries, but that isn’t to say this disparity will necessarily be short-lived or cannot diverge further.

In the bond market, there are several notable examples of historically tied relationships that have diverged for far longer than market participants expected due to structural economic shifts. This is known colloquially in trader parlance as a “widow-maker” trade.

For example, in the aftermath of the European debt crisis in 2011, German sovereign bond yields (bunds) and U.S. Treasury yields, which had been historically tied, began to diverge. Many traders subsequently bet on convergence back to historical norms. However, year after year, this divergence only grew, with bunds becoming one of the first bonds in the world to fall into negative interest rate territory in 2016.

While the cause of the divergence is different, rate divergences proving persistent is not a new phenomenon. In the U.S., the political environment could continue to be bearish for bond markets in the near term. Tariffs and trade restrictions would likely be inflationary, leaving the Fed with less room to reduce interest rates, while pro-growth policies by the Trump administration such as deficit spending, tax cuts and deregulation could lead to an increase in the term premium (the excess return that investors earn by holding longer-dated bonds).

In Canada, conversely, there is a case to be made for bond bullishness to continue in the near term. The federal government has changed its position and committed to reducing immigration numbers in the years ahead, a policy which is likely to continue after the federal election if the Conservatives come into power in 2025. While we may see some positive effects from a reduced rate of immigration and population growth, such as higher per-capita GDP growth and some reduction in the unemployment rate, on aggregate, a policy of population decline will likely be negative for economic growth. A falling population is likely to put downward pressure on aggregate demand and prompt the central bank to continue to lower rates to support an already weak economy.

The Case for Convergence

Looking ahead, while the current divergence in interest rates, bond yields, currency and economic performance between Canada and the U.S. may continue, in the longer term we believe there is a case for convergence.

From a glass-half-full perspective, Canada has already experienced much of the pain of the BoC’s tightening cycle of 2022–2023. Lower inflation rates and growth in wages in Canada have also meant that real incomes have been rising, which supports the potential for increased consumer activity.

In addition, inflation near BoC targets has enabled the central bank to cut rates significantly. Since monetary policy operates with a lag, these rate cuts are still working their way into the economy and their full impact is yet to come.

Compared to the U.S., not only has Canada had more rate cuts, but the “easing” has been even more pronounced because the Canadian consumer is more interest rate sensitive, particularly to the shorter end of the yield curve, which is the part of the curve where rates have fallen the most.

The typical Canadian fixed mortgage term of five years is set based on the five-year yield, whereas U.S. 30-year fixed-term mortgages are more sensitive to the long end of the yield curve.

This means that Canadian borrowers are already experiencing some of the easing from interest rate cuts since five-year rates have fallen significantly in Canada, whereas 10-year U.S. Treasury yields have increased despite the Fed cutting rates in three successive meetings from September to the end of 2024.

Another case for convergence is that the looming trade uncertainty and tariff policies may ultimately be less significant than currently expected. The Trump administration may be reluctant to impose significant tariffs that are, on balance, damaging to both its constituents and to asset prices. Tariffs or the threat of tariffs may instead become a means to an end to achieve other policy goals.

We will continue to closely monitor the changing U.S. landscape, especially for important policy changes that can affect both the Canadian economy and our Beutel Goodman fixed income strategies.

When the dust settles, the fact remains that the economies of Canada and the U.S. are inextricably linked. In Part 1 of A Tale of Two Countries, we ended with the adage, “When America sneezes, the rest of the world catches a cold”. This month, we will end on a more optimistic note, remembering that if economic growth continues in the U.S., it could very well be a case of “a rising tide lifts all boats“.

Download PDF

Related Topics and Links of Interest:

©2025 Beutel, Goodman & Company Ltd. Do not sell or modify this document without the prior written consent of Beutel, Goodman & Company Ltd. This commentary represents the views of Beutel, Goodman & Company Ltd. as at the date indicated.

This document is not intended, and should not be relied upon, to provide legal, financial, accounting, tax, investment or other advice.

Certain portions of this report may contain forward-looking statements. Forward-looking statements include statements that are predictive in nature, that depend upon or refer to future events or conditions, or that include words such as “expects”, “anticipates”, “intends”, “plans”, “believes”, “estimates” and other similar forward-looking expressions. In addition, any statement that may be made concerning future performance, strategies or prospects, and possible future action, is also forward-looking statement. Forward-looking statements are based on current expectations and forecasts about future events and are inherently subject to, among other things, risks, uncertainties and assumptions which could cause actual events, results, performance or prospects to be incorrect or to differ materially from those expressed in, or implied by, these forward-looking statements.

These risks, uncertainties and assumptions include, but are not limited to, general economic, political and market factors, domestic and international, interest and foreign exchange rates, equity and capital markets, business competition, technological change, changes in government regulations, unexpected judicial or regulatory proceedings, and catastrophic events. This list of important factors is not exhaustive. Please consider these and other factors carefully before making any investment decisions and avoid placing undue reliance on forward-looking statements Beutel Goodman has no specific intention of updating any forward-looking statements whether as a result of new information, future events or otherwise.