26 November 2024

Summary

Summary: Responsible investing has emerged as a dominant investment theme over the past decade. In recent years, however, resistance to the goals and objectives of ESG has been growing, and with a new administration incoming in the United States, responsible investing may find itself at a turning point.

By Beutel Goodman’s Fixed Income Team (as at November 1, 2024)

“You are the first generation of investors to understand to include climate risks, but you are also the last generation that can do something to mitigate climate risks.”

Mark Carney, UN Special Envoy for Climate Action speaking at PRI in Person Conference on October 9, 2024.

The PRI in Person event has become an important part of the global investment conference circuit, particularly for those interested in ESG (environmental, social and governance) themes. The annual conference was held in Toronto in October and brought PRI signatories (asset owners and investment managers), as well as regulators and interest groups from around the world together to discuss important issues in responsible investing.

This year, the conference took place amid a backdrop of hurricanes ravaging the U.S. and expectations for more than US$50 billion in damages. According to NASA, the summer of 2024 (June to August) was 0.1 degrees Celsius warmer globally than any summer since its records began in 1880.[1] Climate-related events mean the cost and availability of insurance is a significant issue, especially in coastal areas such as Florida and California.

In addition, the United Nations Environment Programme (UNEP) estimates that by 2030, the financing needs for physical adaptation and resilience in developing countries could increase to as much as US$387 billion annually.[2] To help guide investment dollars in sustainable finance towards resiliency, the Climate Bond Initiative (CBI) has released the Climate Bonds Resilience Taxonomy Methodology. The CBI identified outcomes that are focused on building the resilience of a specific asset or activity, thereby enhancing its ability to withstand climate impacts, as well as outcomes that aim to achieve broader systemic resilience, contributing to the overall resilience of systems and communities.

Investment managers such as Beutel Goodman can also play an important role in the response to climate change; for example, by identifying material physical risks for the companies in their portfolios and engaging with those companies on resiliency, adaptation and mitigation. These topics and engagements are also relevant for fixed income investors, particularly with respect to sovereign bonds.

Stewardship and Engagement

Responsible investing yet again finds itself at a crossroads. Investors have been successful in driving meaningful changes in terms of decarbonization commitments from corporations, but that can only move the needle so far. There remains a substantial gap between what governments have promised to do and the action they have taken to date. The UNEP recently reported that as things stand, current nationally determined contributions (NDC)[3] under the Paris Agreement put the world on track for a global temperature rise of 2.6° to 2.8°C this century.[4] Additionally, policies currently in place are insufficient to meet even these NDCs. If nothing changes, the world is heading for a temperature rise of 3.1°C. This challenge was addressed at the conference, with speakers discussing the role investors can play in engaging on public policy.

On a positive note, based on the companies that were part of their assessment, Climate Action 100+ found the following:

- 90% disclose evidence of board-level oversight of the management of climate change risks;

- 88% are publicly committed to the recommendations of the Task Force for Climate-related Disclosure (TCFD) or International Sustainability Standards Board (ISSB); and

- 80% have set an ambition to reach net zero by 2050 or sooner that covers at least their Scope 1 and 2 GHG emissions.[5]

Now that is in place, the focus of investor engagement is pivoting to the pathway to net zero, as well as to the disclosure of Scope 3 emissions, the setting of medium- and long-term science-based targets, green-aligned capital expenditures, and the incorporation of a just transition. Climate Engagement Canada plans to release an update on its benchmark results in November.

Investor engagement with sovereigns is more challenging. The only investors with skin in the game are debt investors and their engagements are typically limited to the provincial/state and federal ministries of finance. However, a call to action was made at the conference, urging investors to provide an effective counterpoint to significant government lobbying from the fossil fuel companies. To aid investors, the PRI set up the Collaborative Sovereign Engagement on Climate Change. The initiative’s aim is for investors to work collaboratively to support governments to mitigate climate change, in line with institutional investors’ fiduciary duty to mitigate material financial risk. The group undertook a sovereign pilot program in Australia, engaging on the federal and state level, as well as with the national regulators. The 25 participants found the entities generally welcomed the engagement. Any tangible success in terms of emissions reductions may take longer to play out, but the group did help inform the development of Australia’s new green bond framework.

At Beutel Goodman, we do engage on the federal and provincial level, mainly with the finance departments. Topics we engage on include:

- Physical risk and emergency preparedness;

- Housing affordability;

- Risk of increasing utility costs from the energy transition;

- Impact of increased immigration; and

- Sustainable and green bond frameworks.

We selectively support initiatives and respond to information requests. During Q3/2024, we participated in a public consultation providing feedback via a third party on the Competition Act’s new greenwashing provisions. We also actively participate in working groups that help influence policy, such as the Bank of Canada Canadian Fixed Income Forum – Sustainable Finance Virtual Network.

Climate Transition Plans

On a panel about transition at the conference, the Senator for Quebec (Bedford), Rosa Galvez, stated that transition has shifted from a marathon to a sprint, and we are late to the starting line. Making a corporate commitment to net-zero GHG emissions by 2050 is a good start, but having a credible climate transition plan that aligns with the goals of the Paris Agreement is key. According to CDP (the non-profit that runs the global disclosure system for investors, companies, cities, states and regions to manage their environmental impacts), only 22% of the companies that disclose to CDP have a climate transition plan.[6]

CDP has developed 21 key climate transition plan indicators to aid investors in assessing the credibility of their plans. Only 2% of companies that have a transition plan are currently disclosing on all 21 indicators. The Transition Pathway Initiative (TPI) provides research and data on publicly listed equities, corporate bond issuers and sovereign bond issuers to help investors assess companies’ governance and management of their carbon emissions, as well as to evaluate whether their future emissions are aligned with international climate targets and national climate pledges. TPI also provides sector assessment reports. Canada launched a Canadian Transition Task Force that will establish criteria and expectations for credible and science-based climate transition plans across the Canadian economy. The Task Force is not backed by the government, however, but by a combination of charitable foundations and non-governmental organizations (NGOs) in Canada.

At Beutel Goodman, we recognize the importance of achieving the goals of the Paris Agreement to facilitate long-term financial sustainability. We engage with management teams and boards on their commitment to net zero by 2050, as well as their role in the energy transition. A description of our strategy is detailed in our 2023 Climate Report.

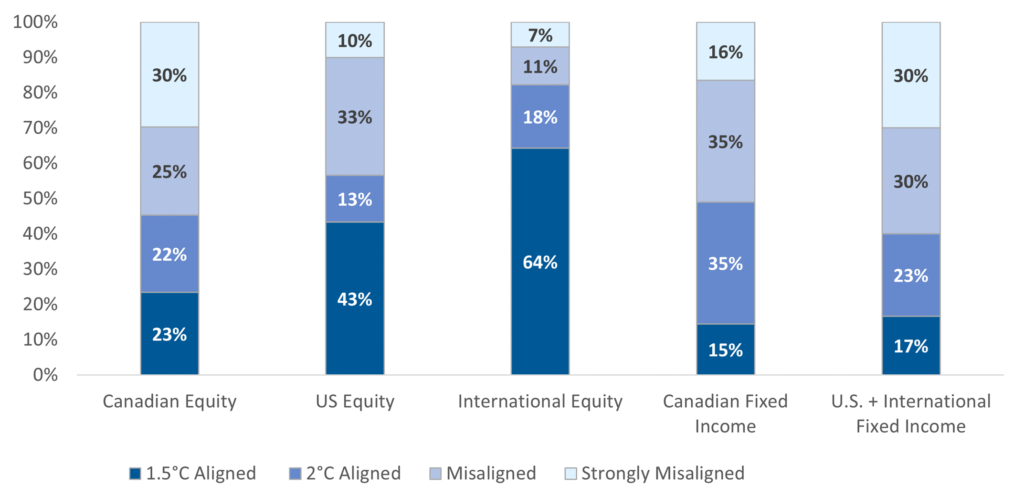

Exhibit 1. Beutel Goodman Portfolios – Alignment to Net Zero.

Sources: MSCI ESG , Beutel, Goodman & Company Ltd. As at December 31, 2023.

Canadian Taxonomy

In a highly anticipated address, the Deputy Prime Minister and Minister of Finance of Canada, Chrystia Freeland, introduced the “Made-in-Canada” taxonomy at the conference. As a backgrounder, the Sustainable Finance Action Committee (SFAC) had published the Canadian Taxonomy Roadmap report in March 2023. The comprehensive report provided a framework and recommendations for a transition taxonomy but required acceptance from the government. A taxonomy provides investment guidelines that categorize investments based on scientifically determined eligibility criteria that are consistent with the goal of reaching net zero by 2050 and limiting a rise in global temperature to 1.5°C above pre-industrial levels.

Canada’s new voluntary taxonomy plan calls for two categories, green and transition, that reflect the energy-intensive nature of the Canadian economy. The green taxonomy focuses on low- or zero-emitting activities, such as green hydrogen-, solar- and wind-energy generation, or those that enable them, such as electricity transmission lines and hydrogen pipelines. The transition taxonomy focuses on decarbonizing emission-intensive activities that are critical for sectoral transformation and consistent with a net-zero, 1.5°C transition pathway, such as installing lower-emitting electric arc furnaces to produce steel.

In the discussions leading up to the development of the taxonomy, the role of natural gas was an intensely debated topic. In the framework, only efforts to decarbonize existing natural gas operations or to replace more polluting fuels abroad (i.e., LNG) could potentially qualify. New projects that increase natural gas production are likely to be excluded. There was no mention of nuclear in the taxonomy backgrounder, but we believe that nuclear power plays a critical role in the energy transition and that Canada could be a leader in the development of Small Modular Reactors. The framework also includes “do no significant harm” criteria addressing environmental, social and Indigenous objectives concurrently.

While the release of the taxonomy framework is an important step forward, we believe there was a significant lack of detail presented at the conference. An independent, third-party organization will be set up to develop eligibility criteria for the following priority sectors: electricity, transportation, buildings, agriculture and forestry, and manufacturing and extractives (mineral-extraction processing and natural gas). The aim is to have criteria for the first two to three sectors released within 12 months.

Two key questions remain. First, is there enough pertinent information in the taxonomy framework for the development of a transition bond market in Canada? The answer is likely no. Sector details and criteria will likely be necessary for that to develop. There is a need for transition financing, as the SFAC estimates that Canada’s climate investment gap is approximately $115 billion annually. The second question is whether the implementation of the taxonomy will survive a potential change in government. The next Canadian federal election is scheduled for October 2025, and current polls have the Conservative Party of Canada in the lead.

A Just Transition

As the conference was held in Canada, there was also a discussion about the just transition, specifically involving Indigenous communities. The path to net zero in Canada runs through Indigenous lands. This would entail the inclusion of Indigenous partners in new projects, as well as the provision of apprenticeship and employment opportunities and Indigenous business procurement. It also includes easing the impact on communities that are reliant on the fossil fuel industry during the energy transition as oil, coal and natural gas production is phased out.

During the Climate Engagement Canada (CEC) panel at the conference, it was stated that only 5% of reporting companies in Canada discuss plans involving a just Indigenous transition, so investors can use the power of engagement to encourage companies to adopt these plans. There are several examples of reputational damage incurred by companies who inadequately consulted with Indigenous communities on their projects. These include Kinder Morgan on the TMX pipeline project and Enbridge Inc. on the Northern Gateway pipeline project. Kinder Morgan ultimately sold the Trans Mountain Pipeline and the TMX project to the Government of Canada, while Enbridge cancelled the Northern Gateway project. Helpful guidance when assessing companies’ consultations with Indigenous peoples includes understanding both sides of the issue and the make-up of the groups involved (e.g., were all the Indigenous involved consulted?), and determining if Free, Prior and Informed Consent[7] was obtained.

The Truth & Reconciliation Commission of Canada’s report lists 94 Calls to Action that government, educational institutions, regulating bodies, religious institutions, and the business community can take “to redress the legacy of residential schools and advance the process of Canadian reconciliation” with Indigenous peoples, with Call to Action #92 setting out specific recommendations for the corporate sector. At Beutel Goodman, we are dedicated to answering the call to action through a number of initiatives. Indigenous relations are also one of the topics on which we engage with our portfolio companies as part of our responsible investing .

Lessons for an Investment Manager

Overall, the PRI conference provided a useful forum for the exchange of best practices on investor engagements. The topics discussed were both interesting on a macro level but also strategically relevant to managing our investment strategies. At Beutel Goodman, we integrate ESG considerations into our investment process to help us evaluate the long-term financial sustainability of a business.

Climate change is a key factor within our responsible investing approach. While considering the climate-related risks facing companies, as part of our research and valuation process we also take into account climate-related opportunities for companies whose business activities and technologies can contribute to the transition and achievement of climate goals.

Climate change is already affecting a wide range of industries, most notably the energy sector, but also insurance, real estate, construction and travel, among many others. The implications are material and something all businesses and investors should consider when planning for the long term.

Setting and following through on goals related to climate risks and opportunities is especially challenging in Canada where the economy is deeply rooted in resources, but as an investment manager, we are committed to engaging with companies in our portfolios on these important topics and goals toward long-term financial sustainability.

[1] https://www.nasa.gov/earth/nasa-finds-summer-2024-hottest-to-date/

[2] https://www.unep.org/resources/adaptation-gap-report-2023

[3] Under the 2015 Paris Agreement, countries must submit plans and targets to cut greenhouse gas emissions as their contribution to reducing climate change called nationally determined contributions (NDCs).

[4] https://www.unep.org/news-and-stories/statements/emissions-gap-report-2024-press-statement

[5] https://www.climateaction100.org/wp-content/uploads/2024/10/2024_10_14-October-Final-Summary-Report-Slides.pdf

[6] https://cdn.cdp.net/cdp-production/cms/reports/documents/000/007/783/original/CDP_Climate_Transition_Plans_2024.pdf

[7] Free, Prior and Informed Consent is recognized in the UN Declaration on the Rights of Indigenous Peoples. It describes processes that are free from manipulation or coercion, informed by adequate and timely information, and occur sufficiently prior to a decision so that Indigenous rights and interests can be incorporated or addressed effectively as part of the decision-making process – all as part of meaningfully aiming to secure the consent of affected Indigenous peoples.

Download PDF

Related Topics and Links of Interest:

©2024 Beutel, Goodman & Company Ltd. Do not sell or modify this document without the prior written consent of Beutel, Goodman & Company Ltd. This commentary represents the views of Beutel, Goodman & Company Ltd. as at the date indicated.

This document is not intended, and should not be relied upon, to provide legal, financial, accounting, tax, investment or other advice.

Certain portions of this report may contain forward-looking statements. Forward-looking statements include statements that are predictive in nature, that depend upon or refer to future events or conditions, or that include words such as “expects”, “anticipates”, “intends”, “plans”, “believes”, “estimates” and other similar forward-looking expressions. In addition, any statement that may be made concerning future performance, strategies or prospects, and possible future action, is also forward-looking statement. Forward-looking statements are based on current expectations and forecasts about future events and are inherently subject to, among other things, risks, uncertainties and assumptions which could cause actual events, results, performance or prospects to be incorrect or to differ materially from those expressed in, or implied by, these forward-looking statements.

These risks, uncertainties and assumptions include, but are not limited to, general economic, political and market factors, domestic and international, interest and foreign exchange rates, equity and capital markets, business competition, technological change, changes in government regulations, unexpected judicial or regulatory proceedings, and catastrophic events. This list of important factors is not exhaustive. Please consider these and other factors carefully before making any investment decisions and avoid placing undue reliance on forward-looking statements Beutel Goodman has no specific intention of updating any forward-looking statements whether as a result of new information, future events or otherwise.

Please note Beutel Goodman’s ESG and responsible investing approach may evolve over time. We do not use ESG factors to pursue non-financial ESG performance. Also note that the integration of ESG and responsible investing considerations into our fundamental research investment process does not guarantee positive returns. Past performance does not guarantee future results.

Certain information ©2024 MSCI ESG Research LLC. Reproduced by permission and subject to the Notice & Disclaimer found at: https://www.msci.com/notice-and-disclaimer; and MSCI Inc’s and MSCI ESG Research LLC’s terms of use at: https://www.msci.com/terms-of-use and additional-terms-of-use-msci-esg-research-llc. No further distribution or dissemination is permitted.

MSCI Fund Ratings are the property of MSCI and provided here for informational purposes only. For more information please see the disclaimer at the end of this document.

Although Beutel Goodman’s information providers, including without limitation, MSCI ESG Research LLC and its affiliates (the “ESG Parties”), obtain information (the “Information”) from sources they consider reliable, none of the ESG Parties warrants or guarantees the originality, accuracy and/or completeness, of any data herein and expressly disclaim all express or implied warranties, including those of merchantability and fitness for a particular purpose. The Information may only be used for your internal use, may not be reproduced or redisseminated in any form and may not be used as a basis for, or a component of, any financial instruments or products or indices. Further, none of the Information can in and of itself be used to determine which securities to buy or sell or when to buy or sell them. None of the ESG Parties shall have any liability for any errors or omissions in connection with any data herein, or any liability for any direct, indirect, special, punitive, consequential or any other damages (including lost profits) even if notified of the possibility of such damages.