10 December 2021

By Beutel Goodman’s Fixed Income team

It is that time of year again when pencils are sharpened and the prognostications for the coming year are rolled out. In keeping with this tradition, we provide our 2022 outlook for corporate credit.

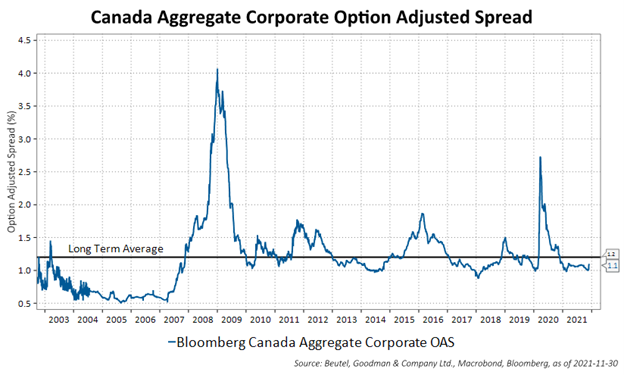

As illustrated in Figure 1, credit spreads have erased all their COVID-19 widening and are through long-term averages. In addition, dispersion amongst credit sectors and credit ratings has narrowed. We believe that credit spreads will remain rangebound into the first part of 2022 before widening in the second half.

There are, however, significant risks to our base-case forecast, and volatility will likely be a key theme for credit markets in 2022. Historically, credit cycles have turned on an event that tends to shock markets into realizing that the lack of differentiation in spreads between sectors and ratings is nonsensical.

Figure 1: This line graph shows that Canadian corporate credit spreads have erased all their COVID-19 widening in 2021. At 1.1% as at November 30, 2021, the option-adjusted spread is through the long-term average of 1.2%.

A Case for Spread Tightening

The economic outlook for credit remains supportive. The Canadian and U.S. economies have likely peaked in terms of economic growth, but that does not mean a contraction is imminent. While growth is slowing, it is still robust. The recovery from the pandemic lockdown has been rapid as various parts of the economy reopen, and the consumer has started spending again. While the recovery continues, though, it has been bumpy due to supply-chain disruptions and the continued spread of the virus and its variants. Overall, we expect that the economy will continue to grow on the back of extensive monetary and fiscal policy stimulus as well as increasing vaccination rates.

On the inflation front, levels have been running high, hitting inflation numbers that we have not experienced in a long time. The key fear for investors is that we are heading for a period of high and persistent inflation like we experienced in the 1970s. In our view, higher inflation will likely be short-lived, as it is fueled by higher commodity prices, supply-chain disruptions and the mathematical fact that year-over-year inflation is coming off a very low, pandemic-fueled base of sub-2%. In fact, two-year core inflation numbers, while they have accelerated over the past six months, are still in line with previous post-recessionary periods in 2002, 2009 and 2015. Inflation readings will likely remain well above 2% into next year, but we expect inflation will likely moderate as the global economy works through its supply issues.

There are also structural elements like demographics that make periods of persistent high inflation unlikely at this point in time. The one caveat is that a trade war, such as a “Made in America” policy, could be significantly inflationary, as the inability to import cheaper raw materials or semi-finished goods make 100%-domestically manufactured goods more expensive. This kind of policy can also lead to retaliatory tariffs with trading partners, which further drives up the costs of goods. Corporate earnings have been strong and for the most part to date, companies have been able to pass along higher input costs. However, they may need to absorb additional cost increases, which could impact margins going forward.

For the better part of two years, companies have been focused on liquidity and balance sheet strength, with growth taking a back seat. Consequently, credit metrics for most corporations are healthy. Credit rating risk has also been benign. Year to date, the average up/down (i.e., the number of credit rating upgrades to downgrades) ratio is 1.87% across the major three credit rating agencies.

Two more technical forces could also create an environment for further credit-spread tightening:

- Corporate pension funded ratios have improved with strong performance in equities as well as higher interest rates, which could lead to an asset-allocation rebalancing into fixed income.

- After two years of strong and above-average new issuance in 2020 and 2021 – driven primarily by liquidity raising, pre-funding and refinancing – a reversion to a more normalized pattern of new issuance is expected in 2022.

The shrinking of net supply coupled with an increase in demand lends support for credit spreads to tighten.

Bondholder Beware

Every credit investor has a wall of worries; it seems to be an inherent part of the job to see risk everywhere. In 2022, one of the key risks for credit markets will be how companies are going to deploy the excess liquidity that was built up during the pandemic. It is likely (and we have already seen evidence of this) that companies will divert cash flows away from debt reduction and towards shareholder-friendly activities such as share buybacks and dividend increases. Growth could also come back into vogue, resulting in an increase in companies’ capital expenditure budgets. Judging from the leverage metrics, “A” rated credits have significant room to lever up, which runs the risk of jeopardizing that “A” rating.

Merger and acquisition (M&A) risk has also been steadily increasing. Between January 1 and November 30, 2021, M&A volume was up 38% in the U.S. and 51% in Canada. For the most part, these transactions have been funded with available cash, equity, and limited debt. A return to highly levered transactions could occur as companies use up their liquidity. For the most part, the leveraged buyout market has been quiet, which presents a risk if cash from private equity is deployed. Break-ups and spin-offs have also been a 2021 trend that is likely to continue into 2022. Where the debt ends up in these transactions creates the risk (or the opportunity) for the bondholder.

Known Unknowns

Additional variants of COVID-19 have the possibility of delaying the recovery in supply chains and improvements in labour markets. There is also the risk that inflation remains stubbornly high for an extended period of time. While ‘transitory’ has many different interpretations, U.S. Federal Reserve (Fed) Chair Jerome Powell’s definition is that inflation won’t be structurally (i.e., permanently) higher. Put differently, the long-run average inflation expectation remains around 2%. The timeline to achieve that average inflation target, however, is an important question for bondholders and is a risk to credit spread volatility in the medium term.

To date, durable goods (e.g., appliances, electronics, autos) CPI has been the driver of the high inflation prints, while services (e.g., transportation, restaurants) CPI has been relatively subdued. The consensus narrative is that as demand for durables recedes, demand will shift more to services, which will lower overall inflation prints.

The risk to this view is the assumption that service prices will stay relatively constant in the face of rising demand. There will be temptation for restaurants, bars, hotels, etc. to raise prices to try and recoup some of their COVID-related losses. This would cause inflation prints to remain higher for longer and is something we are closely monitoring. Lingering inflationary pressures could also start to squeeze margins if companies become unable or unwilling to pass on the price increases, particularly in the consumer goods sectors.

Credit Spreads and Tightening Cycles

Central bank policy will also impact credit markets. Bond markets are expecting that the Bank of Canada will start hiking rates by mid-2022 and are pricing in two rate increases for the year. Generally speaking, credit spreads have performed well during the first phases of a tightening cycle as central banks hike rates as economies strengthen. Credit spreads tend to widen in the later stages of a hiking cycle as negative returns from rising interest rates leads to a sector rotation out of fixed income. A more aggressive tightening cycle (not what markets are currently pricing in) is a risk to credit spreads.

The withdrawal of central bank stimulus could also negatively affect credit markets. The Fed began tapering its balance sheet purchases in November and recent comments from Chair Jerome Powell indicated that the bank may increase the pace of tapering in early 2022. The Fed’s purchases of U.S. Treasuries and MBS created a crowding-out effect forcing bond investors into credit. The withdrawal of monetary policy stimulus could see supporting demand for credit weaken modestly throughout the year.

ESG

ESG will remain topical in 2022. Investment continues to flow into ESG-related funds. On the issuance side, in each of the past several years, the ESG fixed income market has set supply records and we do not expect 2022 to be any different. Green and social bonds are well established, and we expect that demand for sustainability-linked bonds (SLBs) will accelerate next year. In Canada, Telus and Enbridge both issued SLBs in 2021 and we expect several companies are looking at the market, especially those that already have sustainability-linked loans in place.

On the credit analysis side, energy transition risk could start to negatively affect certain sectors such as energy, autos and utilities. ESG disclosure requirements will likely increase, making ESG comparability amongst corporates easier. Corporate bonds that do not have credible net-zero greenhouse gas emissions strategies could come under investor pressure.

Where Do We See Value?

We believe that pockets of relative value remain in the credit markets, specifically in rising stars (issuers that get upgraded from high-yield to investment-grade credit), term loans, different parts of the bank capital structure (LRCNs and AT1s), hybrids, and certain emerging market corporates. Credit-rating agencies were quick to downgrade during the pandemic, particularly in the energy and consumer discretionary sectors. As companies’ credit metrics have recovered strongly and likely faster than the agencies anticipated, several companies are ripe to become rising stars. Currently, we have identified 18 rising-star candidates on our credit approved lists. We also favour overweighting sectors that are still poised to gain from the re-opening (e.g., airlines) and underweighting sectors and companies that do not have pricing power to withstand inflationary shocks and cannot manage/avoid supply chain disruptions. We further note that banks tend to benefit from a rising interest rate environment, which lends support to our current overweight position in Financials.

Portfolio Positioning

While our base-case forecast is for credit spreads to spend the first part of 2022 rangebound before widening again in the second half, we are cognizant of the risks to this thesis. As a result, while we continue to overweight credit in the portfolios, our credit positioning is shorter duration than the benchmark and more defensive. Optimizing roll and carry are also important cornerstones to our corporate-bond strategy. With spreads tight and dispersion low, we expect 2022 will be a credit-picker’s market where playing defense will be rewarded. Ultimately, we believe it is more important to avoid blow-ups than pick winners.

Download PDF

Related Topics and Links of Interest:

- 3 Key Questions for 2022 Answered

- China’s Slowdown: An Aging Dragon Can Still Breathe Fire

- Beutel Goodman Core Plus Bond Fund

©2021 Beutel, Goodman & Company Ltd. Do not sell or modify this document without the prior written consent of Beutel, Goodman & Company Ltd. This commentary represents the views of Beutel, Goodman & Company Ltd. as at the date indicated.

This document is not intended, and should not be relied upon, to provide legal, financial, accounting, tax, investment or other advice.

This is not an invitation to purchase or trade any securities. Beutel, Goodman & Company Ltd. does not endorse or recommend any securities referenced in this document.

The index information contained in this document has been obtained from sources believed to be reliable, but we do not represent that it is accurate or complete and it should not be relied upon as such. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively “Bloomberg”). Bloomberg or Bloomberg’s licensors own all proprietary rights in the Bloomberg Indices. Bloomberg does not approve or endorse this material, or guarantee the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, shall not have any liability or responsibility for injury or damages arising in connection therewith.

Certain portions of this document may contain forward-looking statements. Forward-looking statements include statements that are predictive in nature, that depend upon or refer to future events or conditions, or that include words such as “expects”, “anticipates”, “intends”, “plans”, “believes”, “estimates” and other similar forward-looking expressions. In addition, any statement that may be made concerning future performance, strategies or prospects, and possible future portfolio action, is also forward-looking statement. Forward-looking statements are based on current expectations and forecasts about future events and are inherently subject to, among other things, risks, uncertainties and assumptions which could cause actual events, results, performance or prospects to be incorrect or to differ materially from those expressed in, or implied by, these forward-looking statements.

These risks, uncertainties and assumptions include, but are not limited to, general economic, political and market factors, domestic and international, interest and foreign exchange rates, equity and capital markets, business competition, technological change, changes in government regulations, unexpected judicial or regulatory proceedings, and catastrophic events. This list of important factors is not exhaustive. Please consider these and other factors carefully before making any investment decisions and avoid placing undue reliance on forward-looking statements. Beutel Goodman has no specific intention of updating any forward-looking statements whether as a result of new information, future events or otherwise.